SIP vs FD vs RD – तीनों investment options India में सबसे ज्यादा discuss होने वाले safe + smart wealth parking mode माने जाते हैं। मगर असली reality ये है कि एक middle class Indian, salary based Indian, self employed Indian – सही smart decision सिर्फ data देखकर ही ले सकता है। केवल tradition based logic पर नहीं।

market situation, inflation cycle, tax structure, RBI policy shifts और India की long term economic growth trajectory को देखकर असली सवाल ये है:

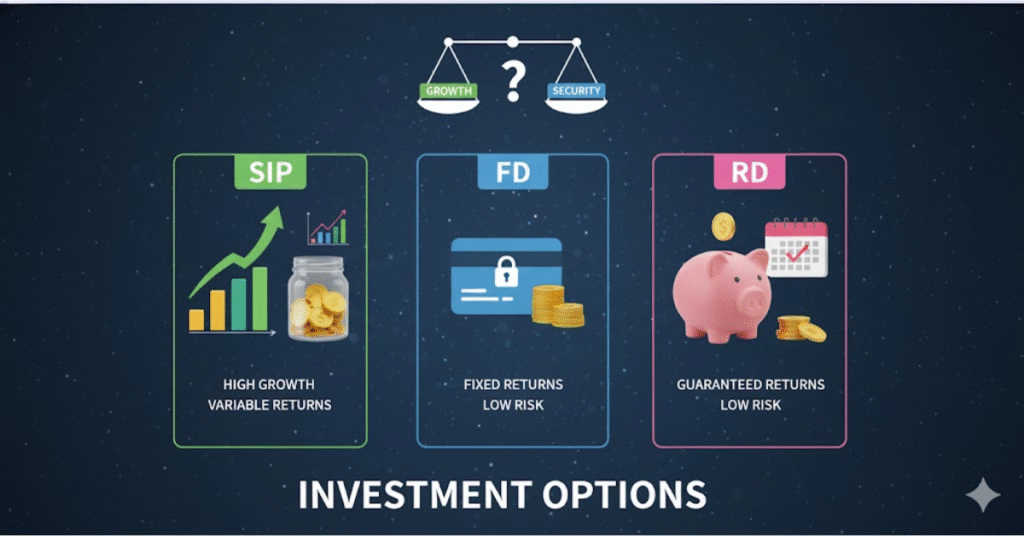

SIP vs FD vs RD

SIP vs FD vs RD में wealth creation के हिसाब से कौन real winner है? क्योंकि India में wealth उसी का बनेगा… जो ये 3 instruments को सही तरीके से अपने goal के according उपयोग करना सीख जाएगा।

SIP क्या है? और क्यों ये future wealth का real engine है?

SIP (Systematic Investment Plan) mutual fund में monthly investment का structured system है, जहां आप ₹500 / ₹1000 / ₹5000 / ₹10000 या जितना comfortable हो उतना amount monthly invest करते रहते हो। SIP का सबसे बड़ा फायदा है – ये market के उतार चढ़ाव को average कर देती है (Rupee Cost Averaging)। इसलिए SIP में time powerful होता है, not timing.

अगर आप 7-10 साल consistently SIP करते हो, तो long term compounding बाकी दोनों FD/RD को बहुत पीछे छोड़ देती है। SIP का असली power short term profit नहीं… बल्कि wealth creation है।

FD क्या है? और ये अभी भी क्यों famous है?

FD (Fixed Deposit) भारत में पारंपरिक safe saving mindset का symbol है। India में parents, relatives, 90% middle class generations FD को safe investment मानते हैं क्योंकि पैसा bank में lock होता है और return fixed मिलता है। FD return approx 6-7.5% के आसपास रहता है depending बैंक + tenure।

But problem? Inflation India में 5% – 6% रहता है। मतलब FD real wealth build नहीं करता, FD सिर्फ safe parking + short term stability के लिए best है।

RBI reference info: https://www.rbi.org.in/

RD क्या है?

RD यानी Recurring Deposit. इसमें महिने महिने पैसे डालते जाते हो। return exactly FD जैसी ही, RD simple disciplined saving habit build करता है, but wealth creation machine नहीं बन सकता, क्योंकि return same inflation के around है।

अब असली Comparison Deep Data Angle (2025 POV)

| Parameter | SIP | FD | RD |

|---|---|---|---|

| Return Range | 12-18% long term (equity) | 6-7.5% avg | 6-7% avg |

| Risk | short term risk high but long term stable | zero market risk | zero market risk |

| Inflation Beat | Yes | No | No |

| Tax Benefit | available Equity MF में better | fully taxable slab | fully taxable slab |

| Liquidity | anytime exit possible | premature penalty | less liquid |

| Wealth Creation Capability | very high long term | low | low |

Conclusion table se साफ clear दिख रहा है – Return, Tax और Inflation को beat करने में SIP ही long term king है।

एक Real Example से समझ लो

अगर कोई 5000 रूपये per month invest करता है 5 साल तक…

SIP 14% CAGR → approx 4,48,000

RD 7% → approx 3,66,000

FD same average → approx 3,65,000

Difference खतरनाक है…

यही gap 10 Years में monstrous हो जाता है।

यानी FD/RD सिर्फ safe storing है

But SIP future money machine है

Tax Angle Biggest Game Changer

SIP (Equity MF) में 1 Lakh profit तक Zero LTCG tax applicable, उसके ऊपर सिर्फ 10%, FD/RD में पूरा interest income slab according taxable, मतलब tax angle भी SIP को और strong बनाता है।

Risk Reality लोग गलत समझते हैं

SIP risky नहीं है…

Short term market movement risky है।

FD/RD safe नहीं हैं…

बस return fixed है, risk inflation दे रहा है जो money को चुपचाप खाता है।

True safe वही है जो inflation + tax के बाद wealth बढ़ाये, और वो SIP ही करता है।

किसके लिए कौन best है?

| Goal Type | Recommended |

|---|---|

| emergency fund | FD |

| 6 से 12 month small goal | RD या Debt MF SIP |

| Retirement, Wealth Freedom, Long Term Goal | Equity SIP |

India Smart Investment Strategy Framework

ये strategy Indian Middle Class के लिए सबसे practical balance है:

- Emergency Money FD में रखो

- Short Small Goals RD/Debt MF में handle करो

- Real Wealth + Future Independence SIP में build करो

इस formula का discipline 5+ years follow कर लिया तो financial freedom automatically start हो jayegi.

Financial Education की जरूरत बहुत ज्यादा है

Most Indians पढ़ते नहीं – बस सुन कर invest करते हैं, और यही biggest reason है की India की maximum earning population wealth नहीं बना पाती।

Share Market properly सीखने के लिए ये Detailed Guide बहुत काम की है:

https://earnandfinance.com/share-market-kaise-seekhe/

knowledge = control

knowledge = confidence

knowledge = better money decision

Final Verdict – SIP vs FD vs RD में Real Winner कौन?

Short Term Stability में FD + RD best हैं, Long Term Wealth Creation में SIP ही real winner है, अगर आप अपने future को financially independent बनाना चाहते हो तो SIP mandatory है, FD/RD सिर्फ support system हैं

Wealth हमेशा TIME + COMPOUNDING से बनती है, और SIP compounding को highest efficient mode में activate करता है।

आगे आने वाले decade में India की wealth cycle SIP driven होने वाली है, जो early start करेगा… वही future में finance class में top पर होगा।

जो सिर्फ safe सोचेगा… वो सिर्फ survive करेगा।

पर जो smart सोचेगा… वो wealth create करेगा।

ये तीनों options life में use करने हैं,

पर उनको सही जगह use करना actual smartness है।